Winners and losers of the latest climate CDP scores

Winners and losers of the latest climate CDP scores

New York, April 2024

This year, we are expanding the CDP Climate Change scores analysis to almost 700 global companies. A few take-aways:

- Haleon, Amazon and EssilorLuxottica all obtain a B for their first submission!

- There is no significant downgrade (1 notch max) among the major companies

-

Many major companies (mainly American) continue not disclosing: for example, Chevron, ExxonMobil, Berkshire Hathaway, Tesla, Charter Communications and others.

- Europe is definitely in advance with significantly more companies scoring A/A-.

- France (CAC40) is leading the pack with almost 70% in A/A- (vs. 35% for the US)

- Obtaining single A is getting harder year over year. Germany is the exception.

- Great momentum for industrial companies with 3x more winners than losers. Healthcare is also showing progress.

- All the utilities are either maintaining their score or being downgraded

- IT companies tend to keep high scores (most are between A and B)

-

Financial companies are very heterogenous with many large swings vs. 2022 (both ways) and still a significant number of companies without score for the past 2 years.

Please feel free to share your comments.

Email

Scaling Up! 🚀

New York, November 2023

In our new release, we are taking one more step to track climate performance of companies at scale

Good news, there is an increasing number of companies disclosing their climate performance due to regulation

in Europe and soon in the United States (still waiting to hear from the SEC!). There are also more

organizations collecting climate data. No doubt that integrating these new data sources will significantly

accelerate our efforts to analyze and benchmark corporates' climate performance but at the same time,

we will have to reinforce control mechanism to ensure data quality and comprehensiveness. That is the journey we

are starting by adding this month 2 new sources : Wikirate and Yourstake.

"Wikirate is an open data platform powered by a global community that collects,

analyzes and shares data on company commitments, actions and impacts on people and the planet."

The platform is really well structured, supported by a team passionate to empower people with open ESG data.

Check their latest dataset Climate 100 GHG Emissions.

"YourStake is a platform that provides Wealth and Asset Managers with tools to take their clients

through a values-aligned investment journey, and is an independent Public Benefit Corporation with

a core commitment to make values-aligned investing personalized, explainable, and transparent"

YourStake made the news early 2023 by releasing a free library of SFDR (Sustainable Finance Disclosure

Regulation) data. Many thanks for this contribution!

Please feel free to share your comments.

Email

Offsetting data now available!

New York, March 2023

New York, March 2023

Thanks to one of our sister websites, Net Zero Tracker (

zerotracker.net), information about the use of offsets and CDR (Carbon Dioxide Removals) in

the net zero targets of

companies is now included on net0tracker. Many thanks! Click on the logos for examples  Microsoft

Microsoft  Netflix

Netflix  Colgate

Colgate

Net Zero Tracker (

zerotracker.net) is a great (and very-much needed) initiative, born out of a collaboration

between research and

non-profit

organisations (Oxford Net Zero, Energy & Climate Intelligence Unit, Data-Driven EnviroLab and

New Climate Institute), with the ambition to increase transparency and accountability of net zero targets. By

collecting data at scale and making them freely

available, they quickly became the definitive repository of net zero pledges for nations, states and regions,

cities and companies. Here's below how Net Zero Tracker (

zerotracker.net) explains offsets, CDR and the reason why separating emission reduction and

removals is important in quality of targets

Offset credits

"Offsetting claims to compensate an entity’s own GHG emissions by accounting for GHG emission reductions

(including

through avoided emissions) or GHG removals achieved external to the actor. This way, the entity claims a

reduced

net

contribution to global emissions through offset credits. Offsetting is typically arranged through a

marketplace

for

carbon credits or other exchange mechanisms."

Carbon dioxide removal (CDR)

"CDR, also known as negative emissions, represents any action that removes carbon dioxide from the

atmosphere.

CDR

comprises a range of nature-based solutions, for example afforestation, or reforestation, and technological

solutions,

for example direct air carbon carbon and storage (DACCS)."

Separate emissions reduction and removal targets

"Some entities differentiate their emission reductions targets from their removals targets. Separate targets

for

emission

reductions and removals improves transparency, making it easier to track progress and compare the level of

target

ambition.

The achievement of the Paris Agreement temperature goals requires both rapid emission reductions and the

removal

of

residual emissions. Separating emissions reduction and removal targets recognises that the outcomes of

removal

activities are generally not equivalent to the outcome of emission reduction activities."

Data source from zerotracker.net - For more information, see

methodology

Please feel free to share your comments.

Email

Surprising insights in 2022 climate scoring

New York, January 2023

New York, January 2023

Here's my observations for the 2022 climate scoring of top 100 companies in the US:

-

Based on CDP 2022 Climate Change questionnaires, scores are getting worse on average with relatively

less companies scoring in A to B- range

(-14pts vs. 2021)

and more in C to D range (+8pts). It is probably due to the evolution of the scoring system more focused

on

accountability than just reporting comprehensiveness. Still 33% companies are scoring A/A- (vs. 42% in

2021).

- Something is happening in the US financial sector: all the major American banks (Bank of America, Morgan

Stanley,

Goldman Sachs, Wells Fargo, US Bank, Capital One, Citi) submitted the questionnaire but were not scored.

According to CDP, these companies submitted their questionnaire after the deadline.

That also explains the drop in A/A- scores vs. 2021.

- Top 3 upgrades are companies that started reporting recently: 2nd year for Meta (B), Booking

Holdings (C)

and first year for Broadcom (C).

- Top 3 Downgrades are ConocoPhillips (B=>D), BlackRock (A=>C) and WalMart (A- =>C). Note that the

scoring details are not publicly available so it's hard to understand the key drivers

- Amazon and Broadcom started submitting in 2022 whereas Netflix and Charter Communications both stopped

after reporting in 2021 for the first time.

And congratulations to the 19 companies that were upgraded. Among them, you will probably hear from companies

reaching

the best score (A) : Cisco, Coca-Cola, Accenture, Linde, Google, Adobe and AT&T.

This analysis is based on CDP Climate Change questionnaire. As of 2023, CDP is the largest database with 18,700+

companies (50%

global market cap) disclosing their environmental performance in 2022. Similarly to a financial rating agency,

each

company receives a score, from A (leadership) to D (Disclosure only) that indicates "the level of action

reported by the

company to assess and manage its environmental impacts during the reporting year".

Please feel free to share your comments.

Email

(Technical) Project Status - Still a Prototype?

New York, November 2022 - Technical Update

During summer 2021, I started developing this website like a prototype, leveraging Django framework (because

I love Python) and a big

Excel file

with CSV extracts to display stats, scores and build charts. On top of learning (thank you

Stackoverflow and all the open source communities) the basics on how to develop a simple website, I spent a

lot of time manually inputting data,

scraping

websites and testing different ideas for scoring.

Early 2022, I realized that this website would be impossible to maintain if I did not fundamentally change

its architecture. The main limitation was my inability to deal with simple time series and score versioning.

Over the past year, here's a status of the main technical changes:

-

KILL THE BIG EXCEL FILE and migrate all data to a POSTGRESQL database. That required re-writing

all the code for querying and computing charts, scores and statistics - it was long but extremely

satisfying. The website became slighlty faster too (postgresql queries are usually faster than

manipulation of a

csv file with pandas). There are now more possibilities for statistics, like computing scores for

different periods or analyzing performance by sector.

-

CREATE A USER INTERFACE FOR DATA INPUT: changing an excel file is far easier than interacting

with a database but it provides very low control on the quality of data input. That is why I created a

separate web interface to input data and load supporting documents, with data checks embedded in the

user input forms. I successfully tested this interface during summer to input new data from

recent sustainability reporting of companies.

-

CREATE A USER PERMISSION SYSTEM AND VALIDATION WORKFLOW: along with the user interface, I had to

create a user permission system to allow users to input data with the possibility to verify data before

they are taken into account for updating scores and statistics of the website. This part still requires

a lot of work before it can be fully functional.

-

SEPARATE FRONT AND BACK-END (as much as possible): technically, I think my architecture is still

monolithic but I separated as much as possible the visual rendering of the website with the back-office

routines (cron jobs mainly) that update the database. It makes the code more readable and maintainable

too. I also separated static (like css or some static pictures) and media files (mainly upload documents

and dynamically-generated charts).

-

DIFFERENTIATE PRODUCTION AND LOCAL ENVIRONMENT: I am the only developer and my website is quite

light in terms of data and code, that is why for long time, I had no issue with working on very similar

environments in local and production. Well... that also caused many problems and security risks!

So What? Why does it matter?

The more I learn, the more I realize how my mistakes could have been easily avoided and how professional

software engineers would have done a way better job BUT I learnt invaluable lessons that can only be learnt

by doing. First, the value of prototyping is huge - by playing with Excel for many months, I could test a

lot of ideas and better define better data models later. By doing it fast, I also maintained my motivation

and was laser-focused on the website objective (not its technical foundations). Then, I realized how easy it

is to fall in love with coding, architecture, lastest tools (there's real beauty in clean code) and get

disconnected with the end objectives...

I experienced it myself so I can also better

understand some software professionals who tend to behave the same way. Finally, I love learning and solving

problems and remembering this journey inspires me, and hopefully others, to continue dreaming developping

bigger things.

What's Next?

By year-end, I plan to update all the 2022 scores and prepare for 2023. Here's the ideas for now:

- Way more analytics

- Study the expansion of the scope of covered companies beyond the S&P 100

- More real-time data (especially finance and economic data) to counter-balance the pretty static scoring

- Open the website to external contributors and users

Please feel free to share your comments.

Email

Climate Performance Reporting

Focus on Progress! First Observations on 2022 Climate Reporting

New York, June 2022 - One year ago, I started analyzing the climate performance of

the top 100 American companies by scanning through their website, sustainability reporting, CDP

disclosures, verification report and updates about their progress to date.

I added additional data points from MSCi (Implied Temperature Rise) and SBTi with the

objective to calculate a global climate performance score that

balances transparency (30%), commitments

(40%) and results (30%). See methodology here (note that the scores will be

updated

after completing all the reviews by early July 2022.).

New York, June 2022 - One year ago, I started analyzing the climate performance of

the top 100 American companies by scanning through their website, sustainability reporting, CDP

disclosures, verification report and updates about their progress to date.

I added additional data points from MSCi (Implied Temperature Rise) and SBTi with the

objective to calculate a global climate performance score that

balances transparency (30%), commitments

(40%) and results (30%). See methodology here (note that the scores will be

updated

after completing all the reviews by early July 2022.).

Over the past 3 months, many sustainability reports were released to the public. Here's my first

observations on 2022 Climate Reporting:

📉Focus is clearly shifting from aspirational goals and compliance to analysis of progress against

targets. We also observe much fewer new targets in 2021/2022. This is consistent with the SBTi project

to better measure progress against stated targets (see SBTI PROGRESS REPORT 2021)

📈More companies report on their climate performance with also better transparency, dedicated

resources

on often revamped sustainability section of corporates websites and much better explanations about methodology,

key figures (providing a full 'ESG data table' seems like a best practice) and alignement with other reporting

frameworks (e.g.

CDP, GRI,

TCFD...).

🔍Better control: the level of third-party external assurance on GHG emissions disclosures

tends

to

increase, with more

companies moving from limited to reasonable assurance (mainly over scope 1 and 2).

🔓Still too many restatements: as companies are expanding the management of their GHG

footprint,

better methodology and calculations are retroactively applied to past years, but usually without an additional

third-party verification.

⌛️GHG reporting is still issued very late compared to financial information. Most climate reporting

are

issued 6

to 9 months after the closing of the reporting period. A few companies started dislosing estimates with

disclaimers.

📊Scope 3 reporting is still very unstable and heterogeneous. In general, more categories are

added

and verified but normalization and good understanding of full value chain performance will remain challenging

until we get

confident about the comprehensiveness of scope 3 reporting. Supplier engagement initiatives are increasing

though.

Please feel free to share your comments.

Email

New SEC Proposed Rules

Better consistency, comparability and reliability

New York, June 2022 - If adopted, the proposed SEC rules related to climate-related

disclosures will

significantly enhance consistency,

comparability and reliability of climate data and risks for almost 7,000 companies in the US. Only a few

days left (until June 17) for public comments.

Let's start with my Top 5 positives ❤️

💡 On top of scope 1 and 2 emissions, scope 3 emissions will have to be disclosed if material or if a

company has

committed to a GHG emissions reduction target that includes scope 3. This is a very smart way to mandate

scope 3

reporting, clarify the scope of net zero commitments for a lot of companies and keep them accountable.

📊 Most of GHG protocol is adopted but not fully: in particular, companies will be required to align

with the accounting

principles of the financial reporting : same fiscal year period, same historical periods, same

organizational boundary

as the consolidated statements… so that analysis of financial and climate performance can be analyzed

together

consistently.

📆 The timing of GHG disclosures will have to align with financial reporting, so companies will have

to

either track GHG

emissions on a quarterly basis or rely on estimates (SEC notes that if actual reported data is not

reasonably available,

a company will be permitted to use a reasonable estimate of its GHG emissions for its fourth fiscal

quarter). Today,

most companies only report on an annual basis with 6-9 months delay compared to financial results

disclosures.

📚 The structure (articulated around governance, strategy, risk management, and metrics and target) and

content of

disclosures (e.g. physical vs. transition risks) are based on TCFD framework, like ISSB, which is

excellent

news.

Disclosures of targets, transition plan, progress vs. plan, associated expenditures (expensed and

capitalized costs),

internal carbon price, uses of carbon offsets and RECs (incl. costs), scenario analysis (if used) will

promote

transparency and peer benchmarking.

✒ Limited assurance (similar to the quality of a financial review) from 2024/2025 and reasonable

assurance

(similar to a

financial audit) from 2026/2027 will be required for the disclosure of Scope 1 and Scope 2 emissions of

large companies.

Smaller reporting companies are exempt.

...and the Top 5 negatives 🤔

🌂 Scope 3 disclosures benefit from a “safe harbor” mechanism, limiting liability exposures. Let’s

hope this

will be

removed soon, at least for the largest companies.

📅 First mandatory climate-related reporting is expected in 2024. This is too late given the climate

urgency

(a good

reminder that SEC mission is not to address climate-related issues but protect investors, maintain fair and

efficient

markets and promote capital formation).

📉 Scenario analysis is not mandated (yet) but required to be disclosed if used. This is an essential

tool

for risk

management that should be integrated in the future.

❓No specific methodology is prescribed for financed emissions (category 15 in scope 3), which will

leave

(too) much flexibility for financial institutions to report on their scope 3 emissions.

💲I am concerned that in the current economic context, the additional compliance costs, estimated at

about

$500k per year, will delay the adoption of this proposed regulation or weaken it.

Please feel free to share your comments.

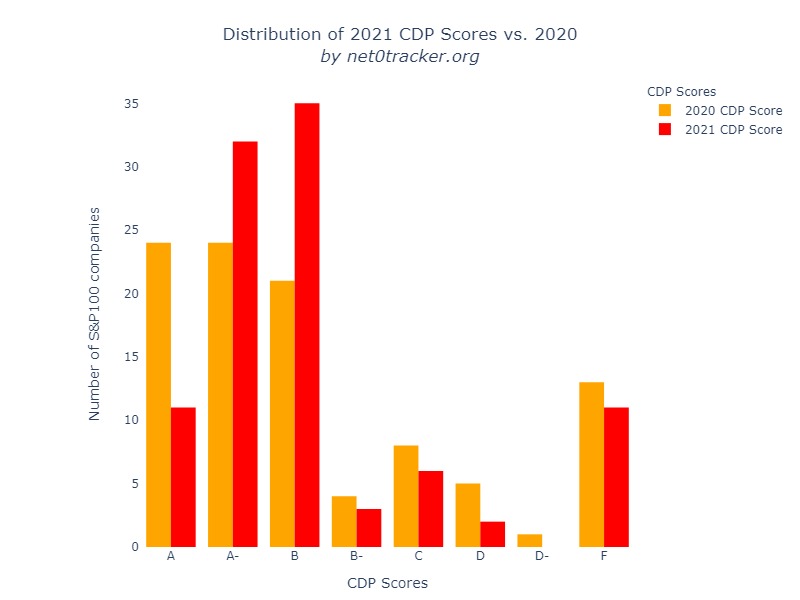

NEW 2021 SCORES RELEASED BY CDP

BETTER BUT STRICTER - MY FIRST LOOK AT THE CDP SCORES (CLIMATE CHANGE)

New York, December 2021 - Here's my first take-aways on the new 2021 CDP scores:

👋 Significant acceleration of disclosures: +35% vs. 2020 (64% market) increase in participation, representing 13,000+ companies worldwide (vs. less than 10,000 in 2020)

✅ Average rating for S&P 100 US companies remain stable at slightly above B-

📶 Single A's are getting more difficult (only 11 vs. 24 in 2020) - the distribution is evolving towards much less A-rated companies and a concentration in A- and B

❌ Among S&P 100, 26 downgrades but by only 1 notch (except Lockeed Martin downgraded from A to B) and usually from high ratings (A / A-).

👍 Among S&P 100, 20 upgrades including many significant improvements due to new-comers like Raytheon (A-), Nextera (A-) but also Starbucks, General Dynamics and American Tower (D to B)

Please feel free to share your comments.

Fight against Climate Change Starts with Transparency (5/5)

10 Best Practices in Climate Reporting

New York, November 2021 - Last summer 2021, I embarked on a wonderful but long adventure : analyzing the climate performance of

the top 100 American companies by scanning through their website, sustainability reporting, CDP

disclosures, verification report and updates about their progress to date. Because there is no public

repository of carbon footprint and climate targets, I had no choice but to manually investigate every

single company based on its public data. I collected over a thousand documents and captured millions of

data points that I intend to make publicly-available on the net0tracker website. My objective was to get

a feel of the state of climate reporting and quantitatively benchmark different companies in their

climate disclosures and performance.

Here's the 10 best practices to improve transparency:

New York, November 2021 - Last summer 2021, I embarked on a wonderful but long adventure : analyzing the climate performance of

the top 100 American companies by scanning through their website, sustainability reporting, CDP

disclosures, verification report and updates about their progress to date. Because there is no public

repository of carbon footprint and climate targets, I had no choice but to manually investigate every

single company based on its public data. I collected over a thousand documents and captured millions of

data points that I intend to make publicly-available on the net0tracker website. My objective was to get

a feel of the state of climate reporting and quantitatively benchmark different companies in their

climate disclosures and performance.

Here's the 10 best practices to improve transparency:

- Provide comprehensive scope 3 footprint data: many companies calculate but do not publish scope 3

data in

their

sustainability report, probably because of lack of verification or trust. Many companies also

misrepresent

the

total scope 3 footprint by only including a few categories (typically business travel and commute).

- Provide all the details of your climate commitments: reduction targets, baseline, scopes,

exclusions

and pace of reduction by year. The formulation adopted by SBTi is a good start.

-

Do not merge scopes or categories: GHG protocol define 3 scopes and specific scope 3 categories for carbon accounting.

Some

companies merge some scopes (e.g. scope 1 and 2) or some categories without providing the details.

- Make the verification report publicly-available: 35% companies claim that their climate

data is

verified but do not provide the verification report.

- Avoid or verify prior year restatements: some companies restate their prior year GHG data, often

because of change of methodology, but fail at making them re-verified by an external

third-party.

- Make GHG data consistent with CDP report: there are still many discrepancies between public

reporting

and CDP report because of periods, scopes or restatements.

- Make CDP report publicly-available: 63% companies provide their CDP report. Since CDP

requires to

create an account and impose quotas on number of companies to search for, a simple link to the CDP

website is not enough to demonstrate transparency.

- Provide the latest CDP questionnaire, even if not available yet on CDP website. The most advanced

companies (14%) share their 2021 submissions even if 2021 scores are not published yet. I also

encourage companies that submit for the first time to CDP (e.g. Netflix, Facebook) to share their CDP

questionnaire

- Publish your climate data in a timely manner: in general, companies report their carbon footprint

6

to 12 months after the closing period, which is still way too late.

- Regularly report on your progress: report on your progress at least on quarterly basis and

provide guidance on the

achievement of your commitments.

Please feel free to share your comments.

Email

Fight against Climate Change Starts with Transparency (4/5)

Do Not Be Fooled By The (CDP) Score!

New York, November 2021 - For most sustainability professionals, the ultimate measure of climate reporting quality and transparency is

the CDP score (climate change questionnaire). It is used by almost 10,000 companies to advertise their

progress

towards environmental stewardship and communicate to investors.

Over the past few months, I have explored the parallels between finance and carbon reporting and realized

that a CDP score is far from telling the full story. Many experienced leaders in sustainability report that

this

score is more related to the completeness of answers to the questionnaire than real climate performance and

carbon emission reductions. But isnt't it natural to think that there is a relation between transparency and

performance? How can we measure this relation?

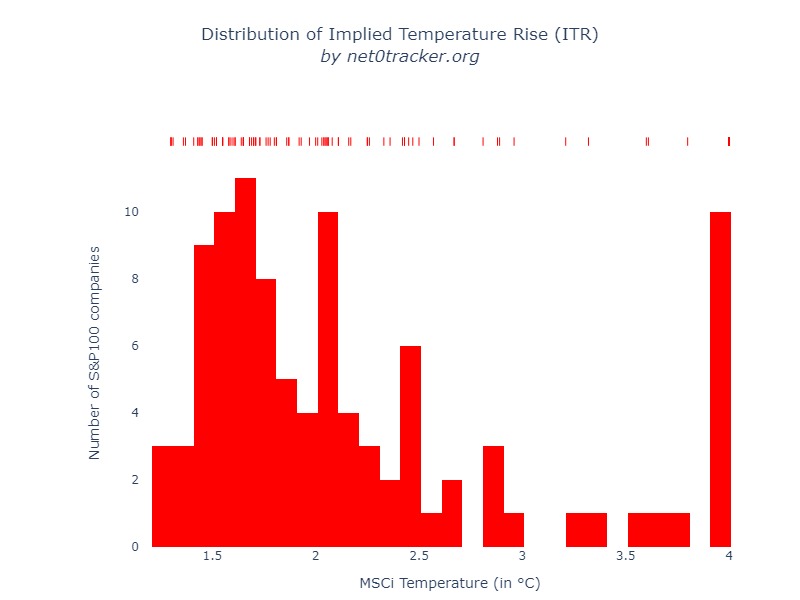

Good news: this week, MSCi made public a new forward-looking indicator to measure the alignment

of

companies, portfolios and funds with global climate targets : the Implied Temperature Rise (ITR). You can now search

over

2,900

companies and check

their ITR and decarbonization target. Thank you MSCi for this contribution!

So let's compare the 2 metrics for the top 100 US companies, starting with the distribution of scores as

shown below.

CDP score distribution is significantly skewed to good scores with 48% and 21% of companies scoring

respectively A/A- and B. ITR score distribution looks similar but proportions are quite different with only

15% of companies below 1.5°C and 38% between 1.5°C and 2°C. This distribution is a sad reminder that despite

all the net zero pledges and alignment to 1.5°C scenario, US companies are very far from being aligned with

Paris agreement.

Let's now plot ITR by CDP score category to understand the relationship.

A few observations:

-

No clear correlation between CDP and ITR scores, even if most of the companies aligning with a below 2°C

scenario have a good CDP score

- Most of C-score companies are below 2°C (AIG, Paypal, Verizon, McDonald, Target, Comcast)

- F-score companies (no CDP reporting) show a few surprises: Berkshire Hathaway and Tesla respectively show a 2.25°C and 2.81°C alignment but do not disclose any carbon data. Facebook and Netflix (committed to reporting to CDP this year) are well

below

2°C. Could Charter Communications (1.7°C) be the next

one?

- High temperatures (>3.5°C) are among all the CDP scores categories: General Motors (A / 4°C), Southern

Company

(A- / 4°C), Dow (B / 4°C), Kraft Heinz (B- / 3.8°C), General Electric (D / 4°C), Nextera Energy (F /

3.61°C) and

Exxon

Mobil (F / 4°C)

Based on this chart (and a limited number of companies), we cannot conclude that there is a link between the 2 metrics even if transparency

should naturally be correlated with the level of carbon reduction targets and climate scenarios. We should

also challenge the methodology of the new MSCi indicator as some results are surprising (for example,

Microsoft or Tesla).

Please feel free to share your comments.

Fight against Climate Change Starts with Transparency (3/5)

3 Major Challenges in Trusting Carbon Data

New York, October 2021 - Exploring GHG emissions data in a ESG or sustainability report is a very similar experience to reading

financials in an annual report: it is technical, full of footnotes, appendix, references to frameworks (e.g.

CDP, GRI, SASB, TCFD...) and external documents. Like finance, the language makes it hardly accessible to

non-experts.

A major difference with financial reporting is the level of verification and regulation. For non-financial

data, we often talk about assurance, not audit, to name the verification process of disclosures. In the

absence of regulation, many assurance providers have adopted various standards, such as ISO14064-3, ISAE

3000, AICPA, AA100 or proprietary methodology. This naturally leads to a lack of consistency and

comparability across companies.

Today, I see 3 major issues in carbon emissions data reporting:

- Partial disclosure is not good enough: Very few companies (1 out of 6) get value chain or scope 3 emissions

verified, which

usually represent more than 80% total emissions.

- Third-party verification is too light: The vast majority (>90%) of assurance statements are 'limited', a type

of

'negative' assurance, which means that it is expressed in a negative form. For example, in a limited

assurance, the assurer states that it did not find evidence that data is materially incorrect. Not really

re-assuring.

- Performance reporting is not rigorous enough: performance against targets are rarely verified,

some past

period data and GHG emissions baselines can be modified without additional verification and restatements

What's next? In the US, regulation is expected to strengthen reporting requirements for major companies. All

the eyes are now on the U.S. Security and Exchange Commission (SEC) that launched a public consultation

about climate change disclosures in Q1 with the objective to provide guidance about new climate reporting

requirements and standards by end of 2021. On top of more regulation, we will also need to strengthen

standards, mainly on scope 3 reporting (e.g. sectorial approach) and emissions reduction claims (e.g.

criteria for net zero claims). Many initiatives, like

TCFD,

PCAF and

SBTi net zero

standard, will undoubtedly support this movement and make carbon reporting more trustworthy.

Fight against Climate Change Starts with Transparency (2/5)

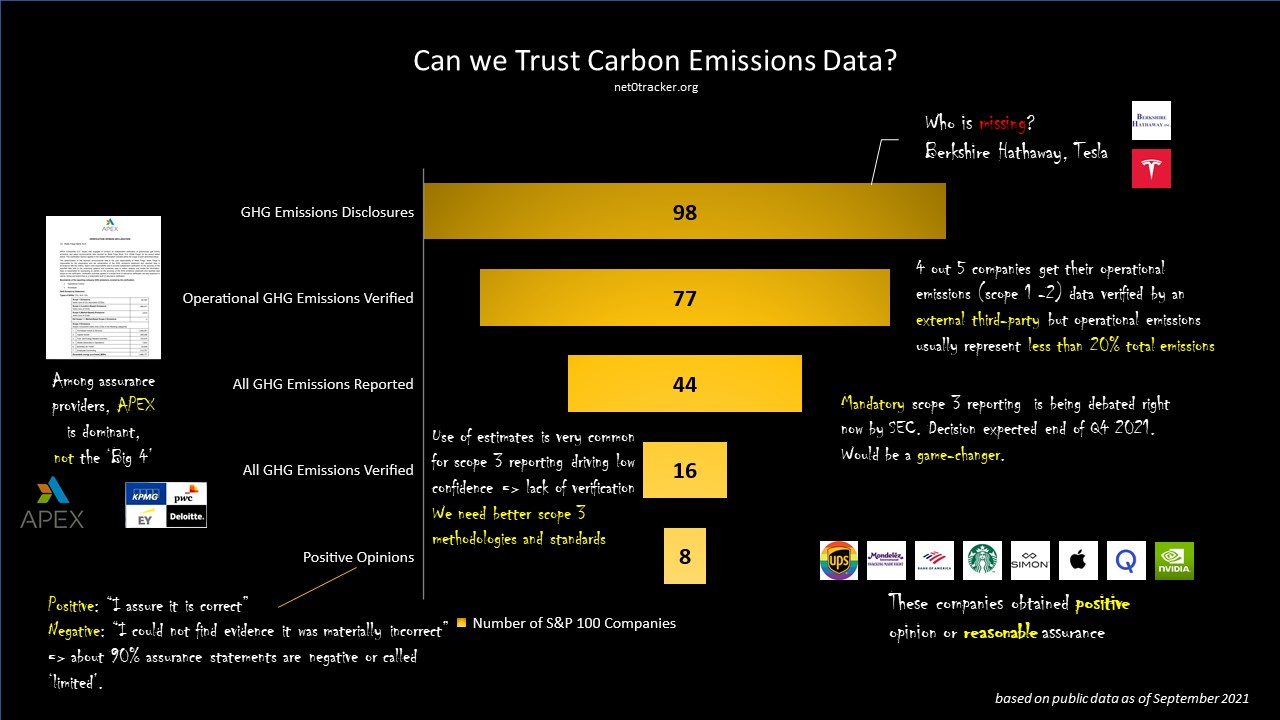

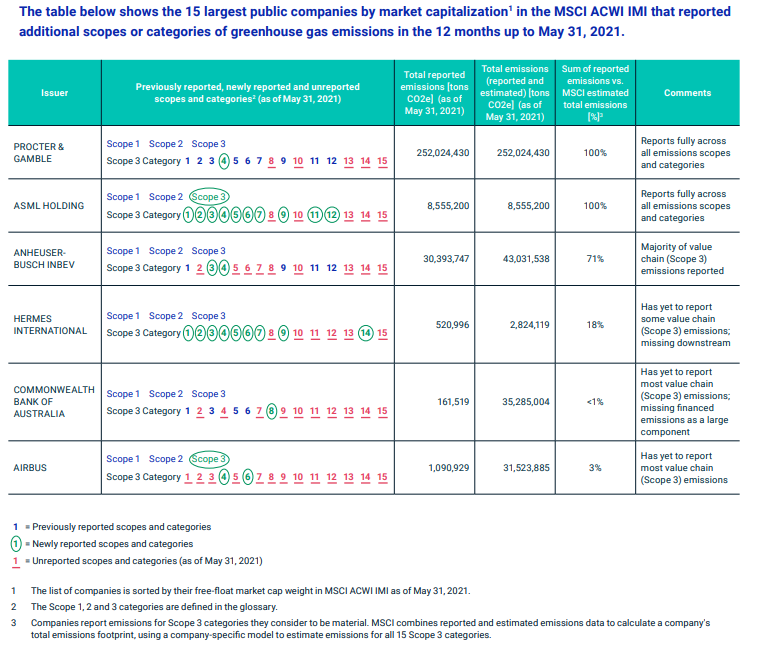

S&P100 companies significantly under-report value chain (scope 3) GHG emissions

New York, October 2021 - In the previous blog, we saw that only 1 out of 6 companies is fully transparent in its

GHG emission reporting, even if about 4 out of 5 companies report scope 1-2 and a part of scope 3

emissions. The real game-changer is the full transparency on value chain (scope 3) GHG emissions.

I estimate that only 44% companies report all scope 3 emissions and only 16% get them fully verified by

an external third-party.

Reporting value chain GHG emissions, both upstream (supply chain) and downstream, remains a

major challenge for most corporates, in terms of data availability, accuracy, consistency, frequency and

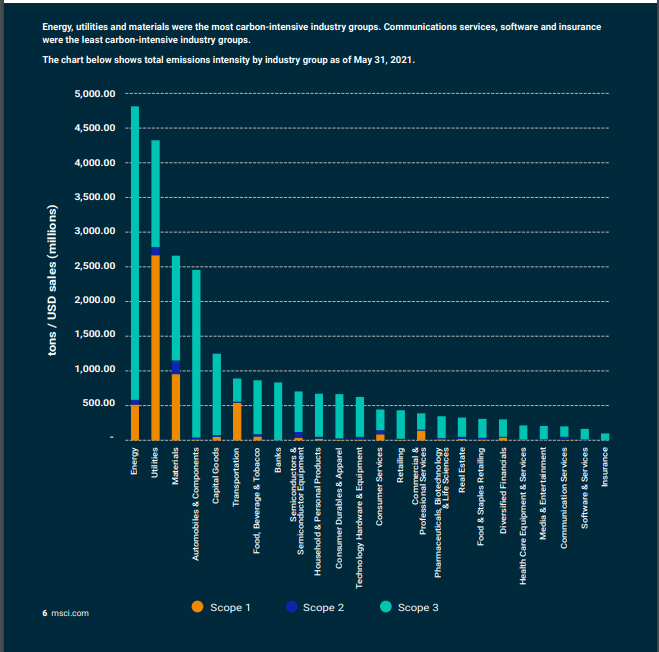

completeness. However, value chain emissions usually represent more than 80% total GHG emissions with

some sectors well-above 90% (for example, 98% in consumer discretionary, 95% in financial services, 94%

in consumer staples). MSCi recently published a study with similar findings (MSCI Net Zero

Tracker), that shows the emissions intensity by scope and

by sector and also tracks the progress in scope 3 reporting.

Among companies reporting incomplete scope 3 emissions, I estimate that about 2/3 scope 3 emissions are omitted on

average. The charts below helps visualize the gap by sector.

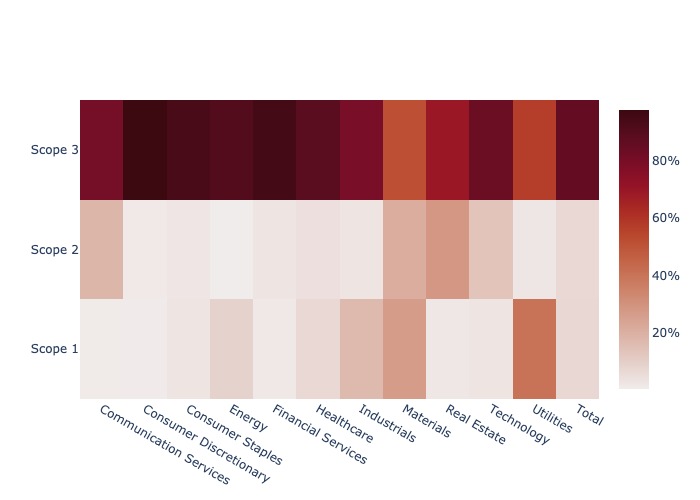

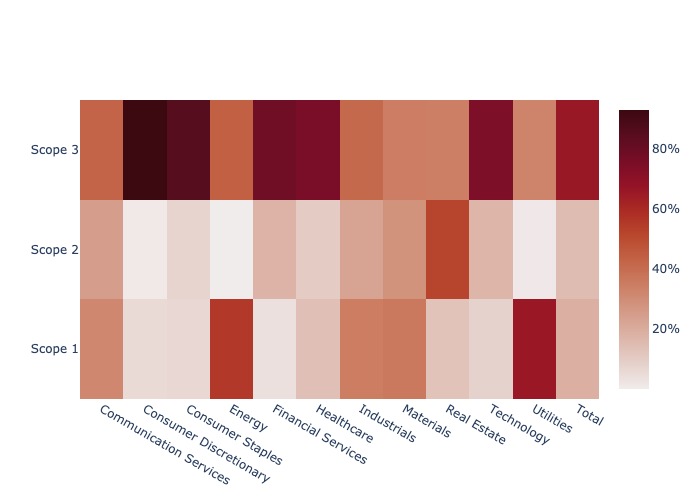

Value Chain Emissions Represent more than 85% of total emissions (vs. 66% are currently reported)

The left chart represents the weight of emissions by scope for companies fully disclosing their emissions. On

average, value chain (scope 3) emissions represent 85% total emissions.

The right chart represents the same as left chart but for all the companies, including those not fully

reporting their emissions. Comparing the 2 charts enable to visualize the under-reported emissions by sector

Note: Only S&P 100 companies (44%) fully disclosing their scope 3

emissions are selected.

Note: Based on all scope 3 emissions reported by S&P 100 companies

Yet, assessing the completeness of scope 3 emissions sounds like a judgement call. Even if CDP requires justification

for every

category of scope 3 emissions (section C6 of CDP questionnaire), companies within the same sector tend to

have different approach or rationale to exclude some categories. This scope 3 completeness issue highlights

the need

for stronger sectorial guidance, methodologies and reporting framework standards specifically focused on

scope 3

emissions. For example, banks tend not to report on scope 15 - Investments because of lack of

widely-recognized methodologies; 3M does an excellent job at reporting their emissions but reports

understandable challenges to calculate product-level emissions (55,000 heavily-diversified products);

tech companies like Amazon and Apple are merging some scope 3 categories (IP reasons?).

In summary: scope 3 emissions are significantly under-reported but there is hope for fast improvements as

many companies are

leading the way in adopting new tools and methodologies to not only demonstrate transparency but also

disclose and optimize the full carbon footprint of their products and services. In terms of timing, I

wish the consumers would get in the game before the regulators!

Fight against Climate Change Starts with Transparency (1/5)

The Big Picture

France, September 2021 - The general public should be able to understand and track the climate performance of companies they work

for

or buy products or services from. Our collective awareness of climate change risks is

going

to intensify in the coming years and new regulations will soon impose more stringent obligations on

greenhouse gas emissions disclosure. Looking at the top 100 largest American companies, what is our

starting

point? How do we define climate transparency? What do Amazon, Berkshire and Tesla have in common?

Transparency refers to clear public disclosures, completeness, timeliness, verification and

quality of climate performance data within generall-accepted accounting frameworks. For GreenHouse Gas

(GHG)

emissions, it means reporting full scope emissions over at least 2 comparable years, fully and

positively

verified by an external third-party, and publicly disclosing supporting materials, such as CDP

questionnaire and verification reports. The level of disclosure is

also

assessed by the CDP score.

Major Companies Failing on Transparency